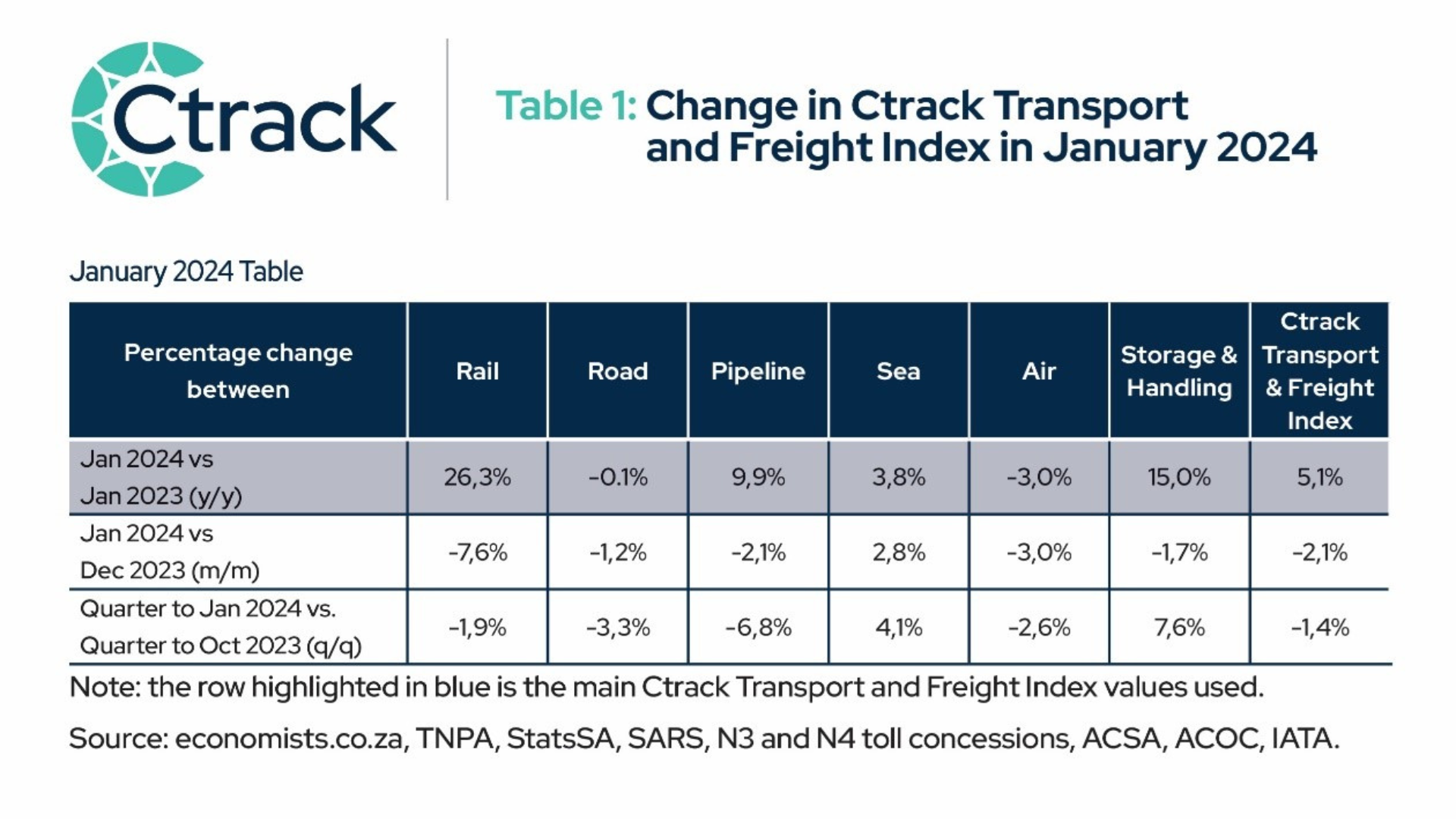

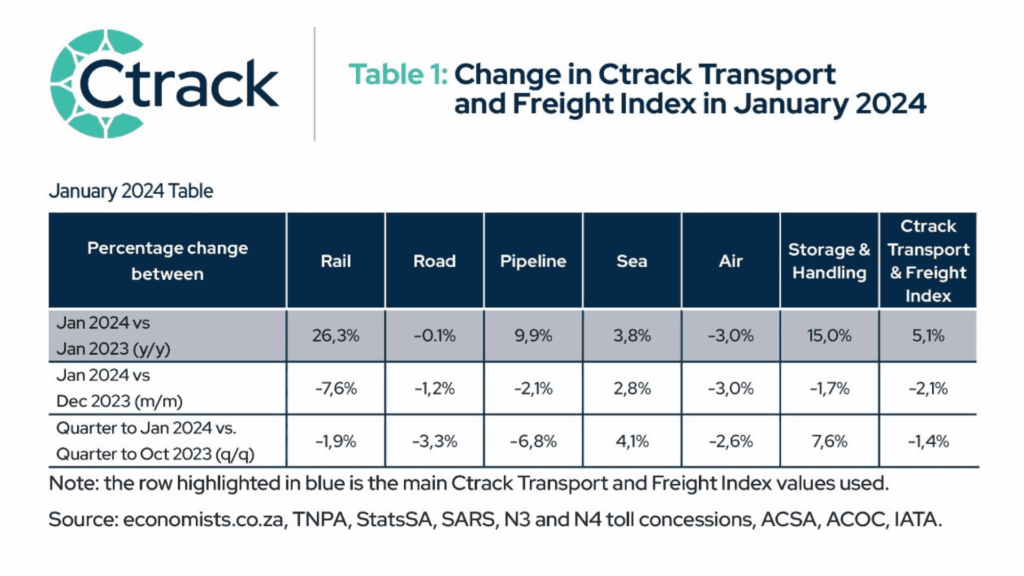

After increasing somewhat in December 2023, the Ctrack Transport and Freight Index (Ctrack TFI) declined notably in January to an index level of 119.3, a drop of 2.1% compared to December’s level of 121.9. The extent of the weakness evident reminds of the pressure the sector experienced amid the KZN looting and flooding episodes – see graph 1. Though the weakness was quite broad-based, the Ctrack TFI is still 5.1% above year-ago levels. The abrupt deterioration in January is indeed a stark reminder that the sector still faces many challenges at the beginning of 2024.

Graph 1: Ctrack Transport and Freight Index – m/m growth rates

Source: Ctrack

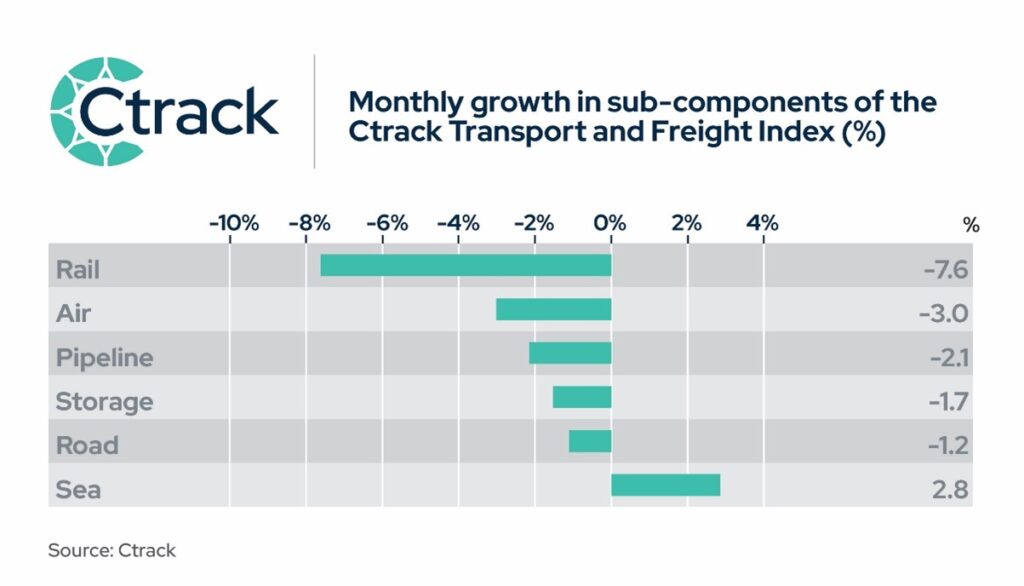

In January, five of the six sub-sectors declined on a monthly basis (see graph 2), with only sea freight expanding. However, compared to a year earlier, four of the subsectors still increased, with only road (only just) and air freight contracting. While the interdependence and intertwined nature of the logistics sector remain relevant as recently witnessed with the implosion of Transnet’s port operations, in January the sector experienced a fairly synchronised decline, confirming the urgent need for structural reform.

Although born out of crisis, some progress has been made towards the end of 2023 to address the sector’s challenges and urgent focus is needed to take these reforms to fruition. According to the latest report from Operation Vulindlela (Q3/Q4 2023) progress has been made in the following areas:

- Approval of the Freight Logistics Roadmap. Working alongside government and Transnet, the Freight Logistics Roadmap was finalised and approved by Cabinet, providing a clear reform path towards resolving immediate operational challenges driving the decline of rail and ports and outlines interventions required to fundamentally restructure the logistics sector through policy and legislative interventions.

- The Minister of Public Enterprises announced the appointment of a permanent board for Transnet National Ports Authority (TNPA). This will replace the current interim board and complete the process of corporatizing the TNPA. The new board will provide critical direction and oversight of the entity as the entire logistics sector undergoes reform.

- The National Logistics Crisis Committee (NLCC) has been formally constituted with participation from relevant government departments, Transnet and business. The NLCC’s objectives are to (i) improve the operational performance of freight rail and ports; (ii) restructure Transnet to ensure its future sustainability; (iii) implement reforms to modernise the freight transport system and restore its efficiency and competitiveness.

- The Economic Regulation of Transport (ERT) Bill has been passed by the National Council of Provinces and public consultation has been concluded. It will now be submitted to the President for assent. Establishing the Transport Economic Regulator is a critical step in the reform of the logistics system.

Graph 2: Monthly growth in sub-components of the Ctrack Transport and Freight Index (%)

Source: Ctrack

Sea Freight remains one of the main focus areas of South Africa’s structural reform efforts. As well-known, in July 2023 Transnet concluded the selection of an equity partner for the Durban Container Terminal Pier 2, which handles 72% of the Port of Durban’s throughput and 46% of South Africa’s port traffic. The partnership will see Transnet Port Terminals enter into a 25-year joint venture with International Container Terminal Services Inc. with Transnet expecting to finalise the agreement by April 2024. The joint venture is expected to crowd in much needed investment and management expertise from the private sector, which will lift the economic value add of the sub-sector and have a broader positive impact on the logistics sector. After tumbling in October and November, reflecting the inability of ports to handle cargo due to a multiplicity of contributing factors, the sea freight sub-component started to recover in December and increased further by 2.8% in January, the only sector to record a positive monthly contribution.

The Road Freight sector, the biggest among the sub-sectors, experienced multiple headwinds in the last few months of 2023 and recorded a slow start to the new year. The road freight sub-component declined by 1.2% in January, compared to December, and slipped marginally below year-ago levels. Heavy vehicle traffic on the N3 route (large and extra-large trucks) declined by 2.6% in January compared to a year earlier, while heavy vehicle traffic on the N4 route declined by 4.6%. Furthermore, total country road freight payload also declined by 4.4% y/y, confirming the broad-based slack in road freight in January, probably a reflection of the mediocre performance of the broader economy.

The Air Freight sub-sector declined by 3.0% on a monthly basis in January, with broad-based weakness evident across all indicators, reversing the recent positive blip spurred by sea freight’s acute troubles. The number of unscheduled flights that are typically chartered for cargo purposes declined by a notable 18.3% m/m in January, while consolidated airport flight movements dropped by 3.7% y/y. Cargo load on planes also recorded a substantial drop in January. The weakness seems to be a localised as globally the air freight sector is still performing well, with multiple demand drivers facilitating an upward trend in air cargo early 2024.

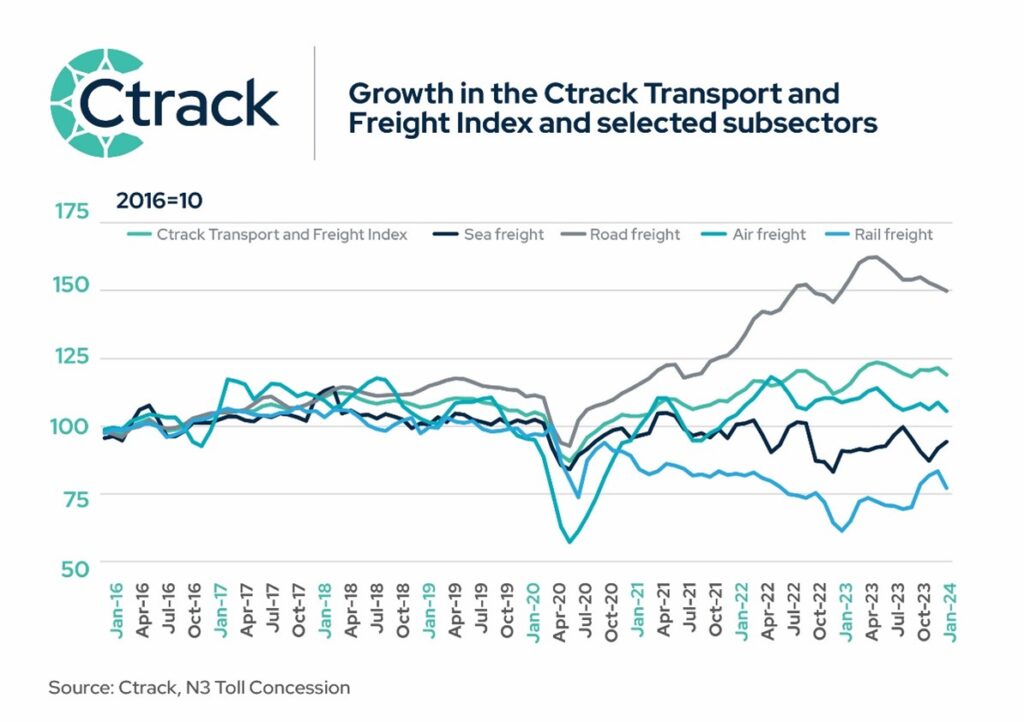

Graph 3 depicts the differential performance among different sub-sectors of the Ctrack TFI. The under-performance of rail and sea freight is evident vs the outperformance of road freight, with notable trend discrepancies evident since the Covid-19 pandemic.

Graph 3: Growth in the Ctrack TFI and selected subsectors

Source: Ctrack

A notable increase in the Rail Freight sub-sector recorded in October 2023 (37.5% m/m) turned out to be short-lived, with the sub-component sagging back to its mediocre levels since then, declining by 7.6% m/m in January, following on sizeable declines in November (-27.5% m/m) and December

(-0.8% m/m). Having been approved by cabinet in December 2023, urgent implementation of the Freight Logistics Roadmap is now needed to improve immediate challenges relating to equipment and locomotive availability, address network security and to facilitate the introduction of third‐party access to the freight rail network, flagged to be executed by May 2024.

The Storage and Handling sub-sector of the Ctrack Transport and Freight Index declined by 1.7% on a monthly basis in January, but remains 15.0% above year ago levels. Total transhipments, both landed and shipped containers, and inventories declined in January 2024, pushing the sector lower. Lastly, the transport of liquid fuels via Transnet Pipelines (TPL) declined by 2.1% in January compared to December, and by 6.8% on a quarterly basis, while this sub-component of the Ctrack Transport and Freight Index still tracks higher on an annual basis (+9.9%).

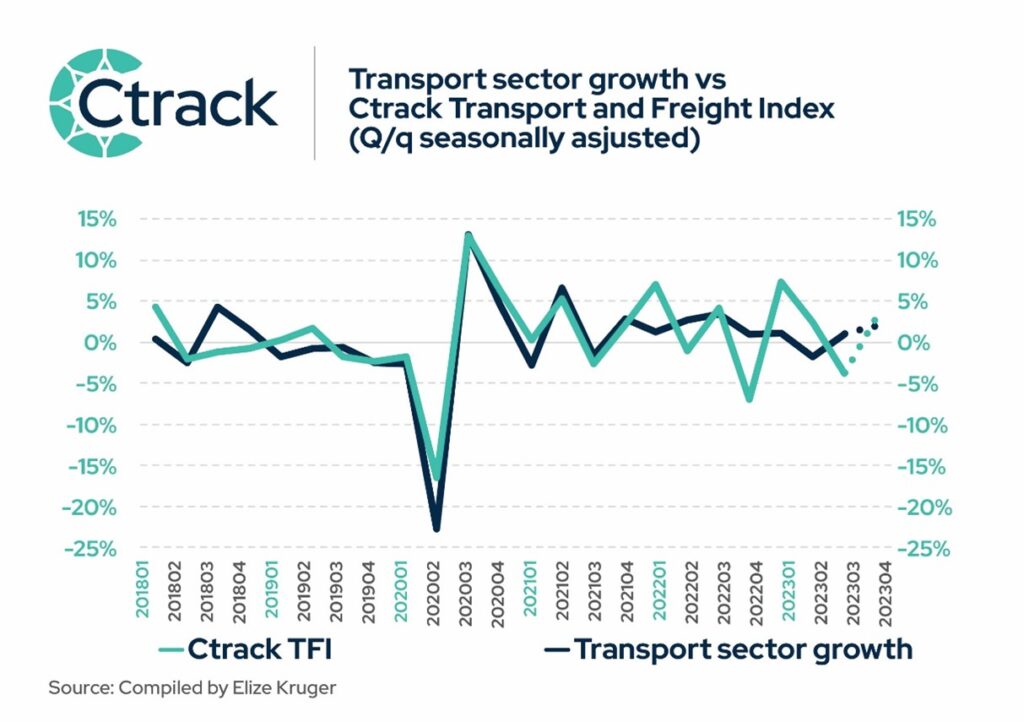

Transport sector to be a positive contributor to Q4 2023 GDP growth

The release of South Africa’s Q4 GDP growth numbers is scheduled for Tuesday 5 March. With the December 2023 Ctrack TFI 2.7% above the September level, all indications are that the transport sector will contribute positively to Q4 2023 GDP growth and will probably also outperform the broader economy that is forecast to grow by only 0.4% q/q and seasonally adjusted. This should seal the full year growth for the transport and communication sector at around 3.5% in 2023, clearly outperforming the broader economy that is forecast to have increased by a mediocre 0.6%.

“The transport & logistics sector is the backbone of the South African economy. The inability to effectively move products to and from markets comes at a cost, which has a negative impact on the whole economy. Not only does it subtract from economic growth, given that products are not timeously available for trading, but the cost of products is typically higher given inefficiencies. An improvement in the efficiencies of the logistics sector could have a multiplier positive impact on the economy as a whole, much needed for South Africa”, says Hein Jordt, Chief Executive Officer of Ctrack.

Table 1: Change in Ctrack Transport and Freight Index in January 2024

For more information or further insights on the Ctrack Transport and Freight Index, feel free to reach out to us at samarketing@ctrack.com or visit our website at www.ctrack.com – Your journey towards a more informed and resilient transport and logistics operation begins with Ctrack.